(408) 357-2733

Calculate Your Solar Installation

There are many different ways to finance a solar photovoltaic (PV) installation. As a homeowner, you may feel overwhelmed by some of the confusing information out there. But because going solar is a substantial investment, it’s important that you understand how each financing option works. Doing so ensures that you receive the highest savings from your clean power investment.

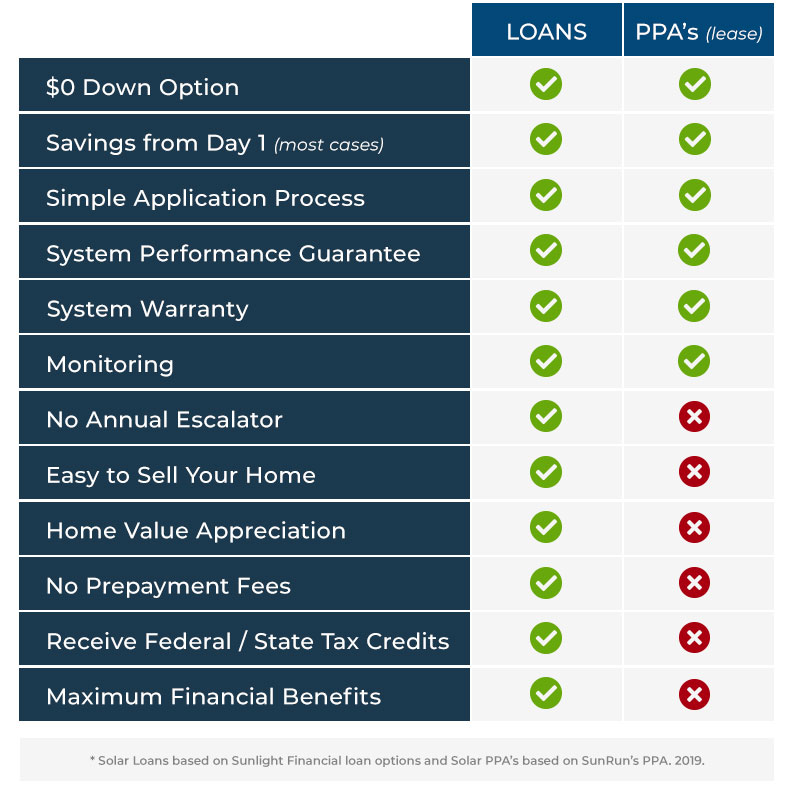

The good news is that the most popular solar financing options share many similarities – whether you’re exploring solar loans or power purchase agreements (PPA’s). We’ll talk about solar leases later, which commonly get misconstrued with PPA’s.

In all 3 cases:

Despite the similarities between solar leases, solar loans, and PPA’s, however, there are crucial differences between how these financing options work.

Let’s dive into a little more detail.

With a Power Purchase Agreement, you pay for the clean solar electricity your PV system generates – at a lower cost per kilowatt-hour (kWh). As such, you enjoy immediate utility bill savings every month.

Many in the industry use the terms “PPA’s” and “solar leases” interchangeably. But there are some crucial differences to how these 2 financing options work:

Here’s an example of how the PPA’s work here at Bright Planet Consulting.

On average, homeowners who choose our PPA option enjoy about 40% savings. With this PPA, you have the option of either:

Agreements typically last anywhere from 10 to 25 years. Once the contract ends, you have the option of either:

Unlike solar PPA’s, you do not face the potential of annual price escalators, and you’re able to receive the 30% Federal Tax credit.

Solar loans are similar to other loans (cars, academic, etc.) With a loan, you:

A Solar Loan Example With Our Preferred Financier

To give you more insight into how solar loans work, we’ll use our preferred solar loan provider, Sunlight Financial, as an example.

With Sunlight Financial’s exclusive solar loans, you get:

Each of the options in this article:

But, for some solar installers, there exists an incentive to install more capacity than the customer really needs. So they may suggest one financing type over the other.

Why?

A larger system means more money – even if the end-user doesn’t need that many panels

At Bright Planet Consulting, we work with you one-on-one to ensure your system is the proper size for you now, and in the future. Not too big, and not too small.

At the end of the day, your solar financing decision should depend on your goals.

If you’d like to discuss which option would fit you best, please book a free, no obligation in-home consultation with us. We’ll discuss past energy usage as well as predictions for the future to determine which solution makes the most sense for you.

Click here to book your free consultation.

To compare solar financing options and see how much you can save, use our solar calculator below.

Calculate Your Solar Savings!Schedule Consultation